4 Reasons not to D.I.Y your pension

We are a nation of DIY enthusiasts.

We spend billions each year tackling household projects and learning new skills in the process.

While DIY is fun and a great way to save money, it can also be reckless & costly – especially if you don’t know what you’re doing.

In some cases, the stakes are low.

For example, it’s not too hard to paint the hallway or fix a leaky tap.

You can always call in an expert to sort it out if you go wrong.

But other jobs, like repairing a gas leak or servicing a boiler, are dangerous if they’re not done by a qualified professional.

The same can be said about your finances.

With more and more DIY pension & investing options available, it’s tempting to have a bash at it yourself.

And, while it can be fun to have a little flutter on the stock market, when it comes to your financial future, it’s best to call in the experts.

Here’s why.

#1 You Could Lose Money and Waste Time

Pensions are a bit more complicated than a patchy paint job.

We’ve met clients who don’t realise things are wrong with their retirement savings until the very last minute.

By then, it can be too late to make any meaningful changes.

For example, one client we know of chose to self-manage his pension, but it wasn’t until he turned 65 and took retirement that he started looking at it seriously.

He soon found himself getting tied up in knots trying to access his pension.

After spending hours and hours on the phone with his provider trying to sort things out, it took upwards of two years to transfer his funds.

He had no choice but to go back to work while things sorted themselves out.

Meanwhile, his portfolio fell in value.

Sadly, these mistakes and issues are common when you try to self-manage retirement savings.

This is why it’s important to work with an adviser.

We’ll create a long-term strategy for your retirement so that you know you’ll have the right money, at the right time.

We’ll arrange all the paperwork and liaise with the providers on your behalf so you don’t have to and we’ll help you feel confident and in control of where your wealth is taking you.

#2 You could be leaving money on the table

These days, you don’t need any special tools to invest in stocks, shares, and hot new financial products like crypto.

Anyone with a smartphone has access to an array of apps designed to make it easy.

But, just because you can, it doesn’t mean you should.

Especially if you wander in blindly without any sort of strategy.

Even if you’re well-informed, and not investing more than you can afford to lose, you still might be leaving money on the table.

Working with an experienced and trusted financial planner on the other hand means maximising your portfolio.

With a deep understanding of the market and the tax-saving opportunities available, we can make your money work as hard as it can for you.

We can also manage your appetite for risk and align your savings with your goals.

We’ll also proactively manage curve balls for you on your behalf – for example, make any necessary changes to your strategy.

In a practical sense, this could mean the difference between your pension providing a pleasant retirement and a luxurious one.

#3 Forward planning and strategy are difficult

Unless you’re trained in financial planning, it can be hard to plan ahead and build a strategy that fits the market.

After all, investments always go up and down.

The past few years have been especially volatile.

Even the best investors saw their portfolios dip. It wasn’t preventable.

What is preventable is ensuring the value of your portfolio doesn’t fall when you need it most.

A good financial planner will have a strategy in place to protect you – and your investments – from market shocks and fluctuations.

This is especially important for your pension when you’re approaching retirement.

Another mistake that clients make is not knowing how much income to take from the pot.

Some clients who manage their own pensions end up taking far too much too early.

Others aren’t taking enough! No one wants to be the richest person in the graveyard – what’s the point of working hard to save for a pension if you die with too much left?

An important part of what we do is helping you balance your income levels so they last.

#4 You’re on your own!

Investing can be scary.

Especially when the markets are performing poorly.

It’s impossible to look at things objectively, without involving your own emotions. This then leads to emotional decisions.

A good financial planner won’t just help you to choose the right things to invest in.

They also offer emotional support when things are turbulent.

Right now, in these turbulent times, good advisers are helping clients to weather the storm, discouraging them from panic-selling stocks and hoarding cash.

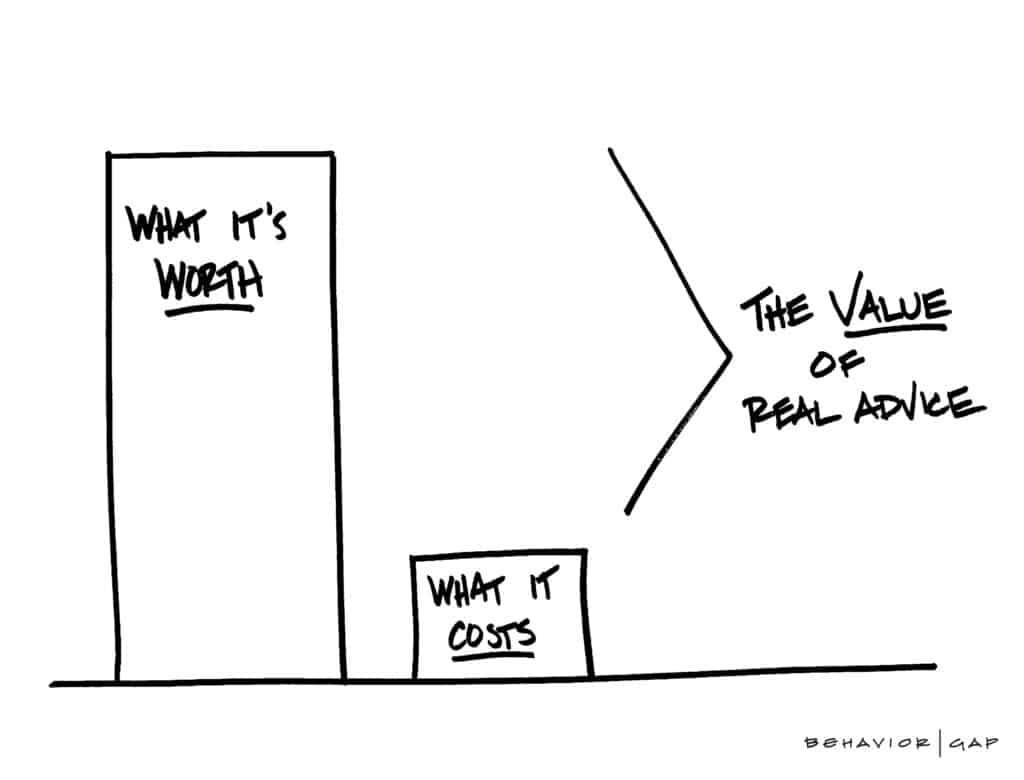

The value of advice

Financial planners add value.

We eat, sleep and breathe personal finance.

We have spent thousands of hours studying and practicing personal finance, you haven’t.

That’s why, when it comes to your finances, like DIY, there is only so much you can do yourself, then you have to outsource.

Russell Investments, a leading investment firm, conducted a ‘Value of an Advisor’ study.

It concluded that advisors delivering a service and value, provided a quantified value of an extra 4.83% per annum.

Vanguard, the second largest fund manager in the world, conducted a similar study.

Conclusion? An advisors value could be quantified at an additional 3% in net returns per annum.

Summary

To summarise, there are a number of pitfalls of doing a DIY job on your pension and investments.

It’s undoubtedly super important to take advice from a fully qualified adviser who isn’t emotionally attached to their money.

Don’t be the client who came to us last year to retire his company pension and it had taken a significant hit due to markets and he wasn’t receiving advise from the scheme advisors.

Yes, advice costs money, but the alternative can be even more costly.

How we help

Do you have a pension and are unsure about how it’s getting on, where it’s invested, how safe or risky it is?

Maybe you have an Approved Retirement Fund (ARF) and are asking the same questions?

How/where is it invested? Am I drawing too much income? Am I drawing enough income?

Maybe your just a DIY investor and want a second opinion to reinforce what you are doing.

Schedule my Financial Planning Consultation

Get in touch

Email us at info@fortitudefp.ie or request a callback.

Alternatively, you can get us on 041 213 0307.

Why not visit our insights?

A multitude of information on various financial subjects covering all aspects of saving, investing, financial planning, protection, and pension advice.

Our blog posts are intended for information purposes only and should not be interpreted as financial advice.

You should always engage the services of a fully qualified financial planner before entering any financial contract.

To discuss engaging the services of Fortitude Financial Planning please email us at info@fortitudefp.ie.

Fortitude Financial Planning Ltd will not be held responsible for any actions taken as a result of reading these blog posts.

Production

Production