Your mindset and goals continually evolve over time.

Both personally and financially.

Financially, at age 25, you might be focused on paying off student loans and saving up for your first home.

Your career is just getting started.

Retirement is way into the future.

At 50, however, you’re starting to imagine a time when the rat race won’t be a part of your life anymore.

And neither will your usual income setup.

Just as your life changes, your investment decisions may develop as well.

If you’re taking the same risky investment approach at age 60 as you did at 25, you may want to reconsider.

And for those who are conservative with decades left until your golden years, you’re most certainly leaving money on the table.

As you move into new life chapters, it’s worthwhile to re-evaluate your investment decisions.

Below we will evaluate how your age can impact your investment decisions.

Schedule Your Investment Consultation

Investment Risks Over Time

Generally speaking, the younger you are, the riskier you should make your investment portfolio.

Earlier in life, many feel comfortable with a high-risk strategy because they won’t be withdrawing for years.

They have time to recover and recoup from any losses from incidents such as a sudden market downturn.

They will be rewarded for enduring market volatility by receiving higher returns.

However, someone who’s a few years away from retirement, won’t have as much time to recover from a plunge in the markets.

Their investment decision should be to maintain a low-risk strategy.

If their portfolio relies too heavily on stocks, their entire retirement strategy could be jeopardized.

Their losses may not be recouped.

If the market corrects close to retirement, their tax-free cash and future income is affected.

Investing At Various Ages

Along with risk tolerance, your age can also be an essential factor when deciding how much to invest and what types of vehicles to invest in.

If you have an investment, you have likely done one of those risk questionnaires.

These assess your risk tolerance.

Risk capacity is as important as risk tolerance.

The younger you are, you have a higher capacity for investment risk.

Particularly with a pension.

This is because you will not be drawing down on it for many years.

For example, the higher the percentage of equities you invest in, the more volatile your portfolio may be in the short term.

But the greater the potential return us.

Many then choose to reduce risk and focus on more steady sources of income as they get closer to retirement.

Investing In Your 20’s and 30’s

After gaining some stability in your life and career, you may be ready to move your money out of a savings account.

Now you should consider a more active role through investing.

Get your money working harder for you.

Read more about investing for beginners here.

With 30-plus years ahead of you before retirement, your intention should be to focus on growth over time.

For those planning on retiring at least 30 years out, it’s common to have upwards of 75% of your portfolio in equities.

For ambitious savers who are interested in retiring early (age 50), you might decide to keep that percentage a bit lower.

During your 20s and 30s, the common investment options include investment accounts and pension schemes.

Learn more about the importance of a diversified portfolio here.

Investing In Your 40’s

As you’re inching closer to those peak earning years, your 40’s can present an opportune time to double down on investment options.

If your employer offers contribution matches to their pension, contributing the maximum amount now could create a promising payout through retirement.

In general, how you invest in your 40’s will vary greatly depending on the types of investment options (if any) that were made in your younger years.

How close you are to retiring and your risk tolerance.

And your risk capacity.

If planning a really early retirement, some people can begin shifting their asset allocation to a more conservative strategy in their forties with stock allocations closer to 65 or 70%.

If retirement is still 20 years away, equities should be your thing.

Investing In Your 50s

How you choose to invest in your 50s will greatly depend on how your current financial picture aligns with your upcoming retirement & financial goals.

Take a look at your current income level, nest egg, taxes and projected retirement income.

This could help you determine how aggressive your portfolio should remain throughout your 50s.

Why? Because now’s the time to focus on creating income for you and your spouse throughout retirement.

Depending on when you plan to retire, today’s 50-year-old man is expected to live an additional 31.9 years, while women can expect an additional 35.3 years.1

Incorporating an appropriate amount of risk into your portfolio can help you and your spouse prepare to experience the kind of retirement you want.

How you may decide to invest throughout your career can be based on a number of factors.

But, it’s always important to take your age and proximity to retirement into account.

As you’re analyzing your portfolio’s asset allocation, diversifying and protecting your future retirement income is essential.

Reflecting on your investment strategies can create peace of mind as you get closer to retirement age.

Summary

Summary

Your age impacts your investment decision.

But it should also impact how you invest.

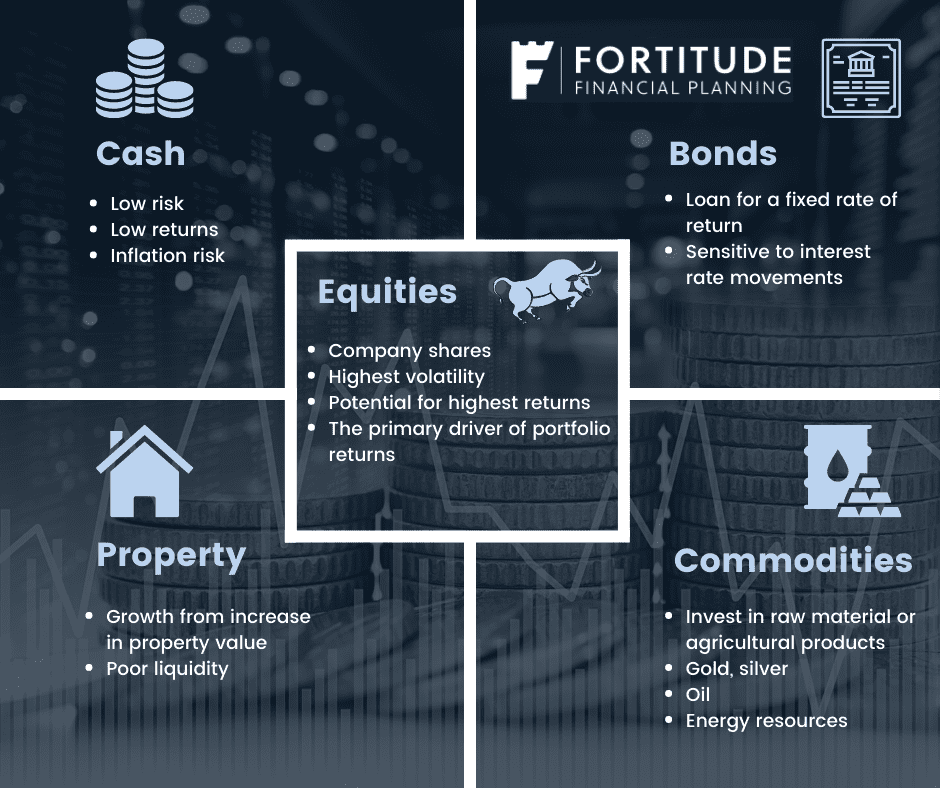

How you allocate your assets between equities, bonds and cash and other asset classes.

The younger you are, the more aggressive you should be – you want growth.

The older you are, the more conservative you become.

In day to day practice I normally see clients becoming more risk-averse as they move through the decades.

This is only natural.

The important thing is your allocation is in line with your own tolerance for risk, capacity for risk and your own individual objectives.

How we help

When it comes to investing there are many considerations.

Both for new investments and existing pensions and investments.

Seasoned investors need to consider these for their investment decisions as well as beginners.

If you have existing investments and want to run a check on them, request a callback or schedule a call for our investment review service.

Not yet an investor but curious as to how it works?

Worried about inflation eating your money?

Request a callback for an informative discussion and we’ll see where you are.

It’s our aim to simplify financial advice for you as much as possible.

We don’t just complete a simple questionnaire and throw you in a risk bucket.

We get to know your objectives and capacity for risk as well as your tolerance so you get the most appropriate advice.

Learn more about our simple investment philosophy here.

Alternatively, call me on 086 0080 756 or drop us an email, info@fortitudefp.ie.

Francis McTaggart CFP® SIA RPA QFA

These blog posts are intended for information purposes only and should not be interpreted as financial advice.

You should always engage the services of a fully qualified financial planner before entering any financial contract.

To discuss engaging the services of Fortitude Financial Planning please email us at info@fortitudefp.ie.

Fortitude Financial Planning Ltd will not be held responsible for any actions taken as a result of reading these blog posts

https://www.ssa.gov/cgi-bin/longevity.cgi

Production

Production